Author: Mohamed Sharfiras

Gazumping and gazundering explained: what every UK buyer and seller needs to know

Gazumping and gazundering are two of the most stressful things that can happen during a UK property transaction. One hits buyers hard, the other can devastate sellers — and both tend to strike at the worst possible moment.

If you’re buying or selling a home in England or Wales, understanding these terms could save you a great deal of money and heartache. This guide breaks down what they mean, when they happen, why they’re legal, and — most importantly — what you can do to protect yourself.

What is gazundering?

Gazundering is the opposite — and it affects sellers. It occurs when a buyer who has had their offer accepted suddenly reduces that offer just before the exchange of contracts, knowing that the seller has already invested significant time, money, and emotion into the process.

The timing is usually deliberate. Buyers who gazunder tend to wait until the seller is fully committed: removal vans may be booked, an onward purchase may be underway, and the entire property chain may be relying on the sale completing. At that stage, the seller faces a painful choice — accept less money or risk the whole deal collapsing.

Like gazumping, gazundering is perfectly legal in England and Wales. A buyer can reduce their offer at any point right up until the exchange of contracts without breaking any law. It’s widely considered unethical, but there is no legal mechanism to stop it.

Why are gazumping and gazundering legal in the UK?

The answer lies in how the English and Welsh property system works. Unlike Scotland — where an accepted offer, once formalised into missives, becomes legally binding much earlier — England and Wales operate on a system where neither party is committed to anything until contracts have been formally exchanged.

This is the exchange of contracts stage, which typically happens after surveys have been completed, mortgage offers have been issued, and solicitors on both sides have finalised all the legal documentation. In practice, that’s often eight to twelve weeks after an offer is accepted — sometimes longer.

During that entire window, either side can walk away without legal penalty. Understanding the full stages of the conveyancing process helps buyers and sellers see exactly where the risks are highest — and how to move through the process as efficiently as possible.

Scotland’s system is often cited as a fairer model. Once missives are concluded north of the border, gazumping becomes a breach of contract. This is why gazumping and gazundering are far rarer in Scotland than in England and Wales.

When do gazumping and gazundering typically happen?

Knowing the timeline is useful for managing your risk at each stage of a property transaction UK.

Gazumping: early to mid-process

Gazumping can happen at any point before exchange, but it’s most common in the earlier stages — particularly while the property is still being marketed as ‘Sold Subject to Contract’ (SSTC). During this period, the estate agent is still legally required to pass on any new offers to the seller, which means a higher bid can arrive at any time.

The risk decreases as the process progresses, but it never disappears until contracts are exchanged. A particularly common trigger is slow progress — if a buyer is slow to get their mortgage offer confirmed or to return paperwork to their solicitor, a seller may decide a quicker buyer is worth switching to.

Gazundering: just before exchange

Gazundering almost always happens at the very end of the process — often just days before the planned exchange of contracts. The buyer waits deliberately, knowing that the seller will be at their most vulnerable. Removal dates may be set. An onward purchase may already be legally committed to. The chain is at risk of collapse if the sale falls through.

Buyers who gazunder are betting that the seller will accept a lower price rather than lose the whole deal. And sadly, given the financial and emotional stakes involved, many sellers do.

The real financial cost of gazumping and gazundering

Beyond the stress and disappointment, both practices can leave you seriously out of pocket.

If you’re gazumped as a buyer, any money you’ve already spent is typically lost. That can include:

- A property survey — often between £300 and £1,500

- Solicitor fees and disbursements, including conveyancing searches

- Mortgage arrangement or broker fees

- Any other preparatory costs such as removals deposits

For sellers who are gazundered, the financial blow comes in the form of the reduced sale price — which could be tens of thousands of pounds less than agreed. If that shortfall affects your ability to complete an onward purchase, the knock-on consequences can be severe.

It’s always worth understanding what conveyancing fees cover so that you can budget properly and know exactly which costs are at risk if a deal falls apart.

Worried about the risks in your property transaction?

Having an experienced solicitor in your corner can make a real difference. From keeping things moving quickly to flagging risks early, the right legal support is one of the best safeguards against gazumping and gazundering. Get in touch with our conveyancing team to find out how we can help protect your position.

How to protect yourself against gazumping

There’s no guaranteed way to avoid being gazumped, but there are practical steps that can significantly reduce your risk as a buyer:

- Move as quickly as possible. The faster you progress to exchange of contracts, the less time there is for another buyer to swoop in. Have your mortgage agreed in principle before you make an offer, and have a solicitor already instructed.

- Ask the seller to take the property off the market. Once your offer is accepted, politely ask the seller to remove the listing. They’re under no obligation, but many will agree — especially if you demonstrate you’re a serious buyer.

- Consider a lock-out agreement. This is a short-term legally binding agreement that prevents the seller from accepting other offers for a defined period. It can provide breathing room while legal work progresses, though not all sellers will agree to one.

- Build a relationship with the seller. A seller who likes and trusts you is less likely to switch buyers for a slightly higher offer. Keep communication open and show that you’re committed and organised.

Look into homebuyer protection insurance. This won’t stop you from being gazumped, but it can help cover some of the financial losses — such as survey and legal fees — if the deal falls through.

How to protect yourself against gazundering

Sellers face a different set of challenges. If you’re worried about a buyer reducing their offer late in the process, here’s how to strengthen your position:

- Keep your paperwork in order from the start. Have your title documents, management pack (if leasehold), and property information forms ready to go. Delays caused by missing paperwork give buyers more time to reconsider.

- Be transparent about the property’s condition. If a buyer later discovers issues they weren’t told about — damp, boundary disputes, planning restrictions — it gives them justification to lower their offer. Full disclosure upfront removes that leverage.

- Maintain communication with your buyer. A buyer who feels kept in the loop and involved is less likely to feel anxious and more likely to remain committed to the agreed price.

- Consider a good-faith deposit. Some sellers request a small, non-refundable deposit from the buyer at the start of the process. This isn’t common practice in England and Wales, but it can demonstrate seriousness and give the buyer a financial reason not to gazunder.

Don’t let the process drag. Market conditions can change. The longer the period between offer acceptance and exchange of contracts, the more time a buyer has to encounter doubts, financial changes, or a shifting market.

Is it different in Scotland?

Yes — significantly. Scotland operates under a different legal system for property purchases. Once a buyer and seller have exchanged formal letters (called ‘missives’) and the terms have been concluded, the agreement becomes legally binding on both sides.

This means that once a deal is done in Scotland, neither party can simply walk away without facing legal consequences. Gazumping and gazundering still occur occasionally — for instance, before missives are concluded — but they are far less common and far less of a structural risk than in England and Wales.

According to The Law Society of Scotland, the earlier binding nature of Scottish property contracts offers considerably stronger protections for buyers and sellers at the offer stage.

Could the law change?

There have been periodic calls to reform the English and Welsh property system to make it more similar to Scotland’s, reducing the window of vulnerability that enables gazumping and gazundering. Various government consultations over the years have discussed introducing reservation agreements, more binding offers, or compulsory processes to speed up transactions.

As of 2026, no legislation has been enacted to make offers legally binding in England and Wales. However, the conversation continues, and some industry bodies are actively pushing for reform. In the meantime, buyers and sellers must work within the current system — and take every practical step available to protect themselves.

If you’d like to understand exactly what happens at each stage of a sale — and where your risks are greatest — our guide to the conveyancing process in the UK walks through the whole journey in plain English.

Buying or selling a property in Manchester? We can help

At Versus Law, our conveyancing solicitors are experienced in keeping property transactions moving — and in protecting our clients when things get complicated. Whether you’re worried about being gazumped, dealing with a difficult chain, or simply want clear advice on your legal position, we’re here to help.

Get in touch today, or use our instant calculator to find out what your conveyancing fees would look like.

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

Estate agent fees explained: what UK sellers really pay

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

Why do people avoid leasehold properties?

Leasehold property problems have driven significant numbers of UK buyers to seek freehold alternatives wherever possible — and the hesitation is understandable. The leasehold vs freehold UK debate has intensified over the past decade as media coverage of escalating ground rents, spiralling service charges, and near-impossible lease extensions exposed a system that had, in some cases, been used to trap homeowners rather than simply govern shared buildings.

That said, leasehold ownership is not inherently problematic. The overwhelming majority of flats in England and Wales are sold on a leasehold basis because the shared nature of a multi-storey building genuinely requires a legal framework to manage communal responsibilities. The issue is not the leasehold tenure itself — it is specific leasehold property problems that arise when ground rents are onerous, service charges are poorly managed, leases are too short, or terms are restrictive in ways that buyers were not properly warned about. This guide sets out the key reasons buyers avoid buying leasehold flat UK transactions, and what to check before you commit.

Leasehold vs freehold UK: what you actually own

The starting point for understanding leasehold property problems is understanding what leasehold ownership actually is. When you buy a leasehold property, you do not own the building or the land it stands on. You own a long-term right to occupy the property for the duration of your lease — typically 99, 125, or 999 years from the date the lease was first granted. The building and the underlying land remain owned by the freeholder (also called the landlord), who retains certain rights and powers for the duration of the lease.

In the leasehold vs freehold UK comparison, this distinction has significant practical consequences. A freehold owner has outright ownership of their property and land in perpetuity. They owe nothing to anyone simply for the right to be there. A leaseholder, by contrast, owes ground rent to the freeholder, must comply with the terms of the lease, requires consent for certain changes, and faces a declining asset as the lease term shortens. The leasehold framework is appropriate for flats — where shared walls, roofs, and communal spaces create genuine interdependencies — but it has historically been applied to houses in ways that many buyers feel were unnecessary and exploitative.

Escalating ground rent: the leasehold property problem that sparked a scandal

Ground rent is a payment made by the leaseholder to the freeholder simply for the right to occupy the land. In the leasehold vs freehold UK context, it has no equivalent in freehold ownership — it is a recurring cost with no service attached to it. For most of the history of leasehold, ground rent was a nominal sum: a few pounds a year, sufficient to acknowledge the freeholder’s residual interest without creating a meaningful financial burden.

That changed in the 2000s and 2010s when a number of developers and investors began using ground rent as an investment vehicle. New builds were sold with ground rents set at £250, £350, or more per year — with review clauses that doubled the amount every ten or fifteen years. A ground rent of £300 per year, doubling every ten years, becomes £2,400 per year within forty years and over £9,000 per year within sixty. Properties with these clauses became difficult or impossible to sell, because mortgage lenders refused to lend against them and buyers recognised the financial trap.

The government responded to this leasehold property problem with the Leasehold Reform (Ground Rent) Act 2022, which abolished ground rent for all new residential leases granted after 30 June 2022, setting it at a peppercorn (effectively zero). However, existing leases with onerous ground rent clauses are not covered by this legislation. If you are buying leasehold flat UK on an existing lease, you need to check the ground rent provisions carefully. Our guide explaining the distinction between chief rent and ground rent sets out how these charges work and what the difference is — particularly relevant if you are buying in Manchester, Bristol, or North Somerset, where chief rents on freehold titles can create additional confusion.

Service charges and the lack of control over building management

Service charges are the annual costs leaseholders pay towards the maintenance of the building and shared areas. In principle, this is a reasonable mechanism for sharing the costs of running a shared building. In practice, service charges are one of the most common leasehold property problems raised by leaseholders — both because of their unpredictability and because of the limited control leaseholders have over how the money is spent.

Service charges can cover a wide range of costs: building insurance, cleaning, gardening, lift maintenance, window cleaning, management fees, and contributions to a reserve fund for future major works. The landlord or managing agent sets the budget and decides what work to commission. While leaseholders have a legal right to challenge charges they consider unreasonable at the First-tier Tribunal, the practical reality is that bringing a tribunal application takes time, money, and willingness to enter into conflict with the freeholder — a barrier that many leaseholders understandably find discouraging.

In buying leasehold flat UK transactions, service charges that have risen significantly in recent years are a particular red flag. Some buildings have seen charges double or triple within a relatively short period, driven by increases in building insurance premiums, the cost of fire safety remediation works, or simply poor management. Before committing to a leasehold purchase, your solicitor should obtain three years of service charge accounts, the current year’s budget, and details of any planned major works — all of which are disclosed through the management information pack requested during the conveyancing process.

Thinking about buying a leasehold property?

Leasehold ownership can involve ground rents, service charges, and restrictions that impact long-term value. Get expert guidance to understand the risks before you commit.

Short leases: the leasehold property problem that makes mortgages impossible

A lease with fewer than eighty years remaining is widely considered a short lease in the leasehold vs freehold UK context — and it creates serious practical problems for both buyers and sellers. Most mortgage lenders will not lend on properties with a lease of less than eighty-five years at the end of the mortgage term. Some require even more. This means that a property with seventy-five years remaining on its lease may be unmortgageable to a buyer seeking a twenty-five year mortgage, effectively making it a cash-only purchase and dramatically reducing the pool of potential buyers.

The solution — a lease extension — is available but expensive. Leaseholders who have owned the property for at least two years have a statutory right to extend their lease by ninety years (for flats) and to reduce the ground rent to a peppercorn. But the cost of that extension is calculated by a formula that takes into account the current ground rent, the length of the lease, and the value of the property — and the shorter the remaining term, the more expensive the extension becomes. The “marriage value” — the increase in the property’s value created by the extension — becomes payable to the freeholder once the lease drops below eighty years, which can add tens of thousands of pounds to the cost.

For buyers considering a property with a lease under ninety years, the cost of a lease extension should be factored into the purchase price negotiation from the outset. Waiting until after completion to address it almost always costs more. A solicitor experienced in buying leasehold flat UK transactions will identify the lease length early, advise on the likely extension cost, and recommend a price negotiation strategy before exchange.

Restrictions, permissions, and the cost of consents

Another category of leasehold property problem that buyers encounter only after they have moved in relates to the restrictions embedded in the lease itself. Leases typically contain covenants — legally binding obligations — that govern how the leaseholder can use and alter the property. These restrictions exist to protect the building as a whole, but in practice they can be unexpectedly limiting.

Common restrictions in leasehold properties include:

- Prohibition on keeping pets, or a requirement to obtain the freeholder’s consent before doing so

- Restrictions on subletting — some leases prohibit subletting entirely; others require landlord consent and impose conditions on any sublease

- Requirements to obtain consent before carrying out any structural alterations, including loft conversions, extensions, or significant internal remodelling

- Restrictions on running a business from the property

- Obligations to seek consent before installing new flooring, particularly hard floors that might transmit noise to lower floors

- Requirements to use the freeholder’s approved contractors for certain works

The process of obtaining consent is not simply administrative. Freeholders are legally entitled to charge a reasonable fee for dealing with consent applications, and what constitutes “reasonable” can be contentious. In the leasehold vs freehold UK comparison, freehold owners can make all of these decisions entirely independently, without paying fees or seeking anyone’s approval. This degree of restriction on what you can do with your own home is one of the leasehold property problems that owners find most frustrating over time.

Fire safety and cladding: the leasehold property problem that emerged after Grenfell

The fire safety crisis that followed the Grenfell Tower disaster in 2017 created a new category of leasehold property problems affecting hundreds of thousands of leaseholders in high-rise and medium-rise buildings across the UK. Buildings found to have dangerous cladding or other fire safety defects required expensive remediation works — and in many cases, the initial expectation was that leaseholders would meet the cost.

The Building Safety Act 2022 introduced significant protections for leaseholders in qualifying buildings, limiting what landlords can recover from leaseholders for historical fire safety defects. However, the situation remains complex. Properties in affected buildings require an EWS1 certificate (External Wall System assessment) before many mortgage lenders will lend on them, and obtaining that certificate — or satisfying its requirements — can take years. This left, and in some cases continues to leave, leaseholders unable to sell or remortgage their homes.

For anyone buying leasehold flat UK property in a building constructed or clad between 1985 and 2020, checking the building’s fire safety status and whether an EWS1 certificate is in place — and what it says — is a critical due diligence step before proceeding.

Leasehold property problems with selling: why resale can be harder than expected

Leaseholders sometimes discover that the leasehold property problems they were not warned about on purchase become the problems they cannot resolve when they want to sell. A lease that was ninety-five years long when purchased is now eighty-two years long ten years later — moving towards the threshold at which lenders and buyers become uncomfortable. Ground rent clauses that seemed manageable have reviewed upwards. Service charge accounts reveal significant arrears or an imminent major works programme that the buyer’s solicitor will flag.

In the leasehold vs freehold UK market, freehold properties generally sell more easily and achieve better prices, all other things being equal. Leasehold properties with anything less than a well-managed building, a healthy lease term, a reasonable ground rent, and clean accounts face a narrower buyer pool and more challenging conveyancing — both factors that affect the price achievable and the time taken to sell.

For sellers, getting a leasehold conveyancing solicitor involved early — before the property is listed — allows time to obtain management information, identify any issues that need addressing, and prepare the leasehold pack that the buyer’s solicitor will require. Understanding what a conveyancing solicitor does at each stage of a leasehold transaction is useful context for both buyers and sellers who want to avoid last-minute surprises.

Should you avoid leasehold properties entirely?

The honest answer is: not necessarily. Leasehold property problems are real and well documented, but they are not universal. A well-managed leasehold flat with a long lease, a reasonable ground rent (or a post-2022 peppercorn ground rent), a solvent and functional sinking fund, and transparent service charge accounts is a perfectly viable purchase. Many people buy leasehold properties — particularly flats in city centres — and have entirely straightforward experiences of ownership.

The leasehold vs freehold UK choice for houses is different. There is no inherent structural reason why a house needs to be leasehold, and the government has moved to restrict new leasehold house sales. If you are considering a leasehold house — rather than a flat — the additional scrutiny is warranted, because the leasehold structure in that context almost always reflects a commercial decision by the developer rather than a legal necessity.

For flats, the question is not whether the property is leasehold but whether the specific lease, building, and management arrangement is sound. That assessment requires professional legal advice, and it needs to happen before exchange — not after.

Getting proper advice before buying a leasehold property

The leasehold property problems that catch buyers out are almost always identifiable before exchange — if the right checks are made. A solicitor experienced in buying leasehold flat UK transactions will review the lease length and ground rent provisions, examine three years of service charge accounts, check for planned major works, assess the management arrangements, and advise you clearly on anything that could affect the property’s value, mortgageability, or future saleability. Knowing the full leasehold property costs you are taking on — not just the purchase price — is the foundation of a sound decision. Our instant conveyancing cost calculator gives you a transparent breakdown of what the legal costs of buying a leasehold property will be, including the additional leasehold fee.

Our residential conveyancing team advises buyers and sellers on leasehold transactions across England and Wales, identifying the issues that matter before you commit and handling the legal work efficiently from instruction to completion. If you have a question about a specific property or want to understand your position before making an offer, get in touch with our team for a no-obligation conversation about your situation.

Need advice on leasehold vs freehold properties?

Many buyers avoid leasehold properties because of high ground rents, short lease terms, and restrictions on changes or resale. Understanding these factors is essential to making a safe property investment. Our conveyancing solicitors guide you through lease terms, potential costs, and legal implications to help you make informed decisions and protect your interests.

-

Gazumping and gazundering explained: what every UK buyer and seller needs to know

-

Home insurance – do I need it?

-

Estate agent fees explained: what UK sellers really pay

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

Home insurance – do I need it?

Home insurance is one of the most important financial protections you can have as a property owner. Whether you’ve just bought your first home or you’ve owned property for years, you may be wondering what cover you actually need, what the law says, and how much it should all cost. This guide explains everything clearly so you can make the right decision for your situation.

Is home insurance a legal requirement in the UK?

Home insurance is not a legal requirement in the UK. There is no law that says you must have it. However, that does not mean you should go without it — and in many situations, you will have very little choice but to take out a policy.

If you are buying a home with a mortgage, your lender will almost certainly require you to have buildings insurance in place before they release the funds. This is a condition of the mortgage itself, not just a recommendation. Mortgage companies insist on it because the property acts as security for the loan — if the building were destroyed by fire or flood, the lender needs to know it can be rebuilt. Without buildings insurance, most mortgage offers will not proceed.

If you own your home outright — that is, with no mortgage — you are free to make your own choice. But the financial risk of being uninsured is significant. A single serious claim for storm damage, flooding, or fire could cost tens of thousands of pounds to put right.

What does buildings insurance cover?

Buildings insurance covers the physical structure of your property. This includes the walls, roof, floors, ceilings, windows, doors, and any permanent fixtures such as fitted kitchens and bathrooms. It also typically covers outbuildings like garages and garden walls.

A standard buildings insurance policy will usually pay out for damage caused by:

- Fire and smoke damage

- Flooding and storm or wind damage

- Burst pipes and water leaks

- Vandalism and malicious damage

- Subsidence, where the ground beneath the property shifts

- Falling trees or debris

It is worth checking the small print carefully. Certain risks — such as gradual wear and tear or damage caused by pests — are usually excluded. If your property is in a flood-prone area or has a history of subsidence, you may need specialist cover on top of a standard policy.

How much should you insure your home for? Understanding rebuild costs

One of the most common mistakes homeowners make is insuring their home for the wrong amount. When it comes to buildings insurance, you should insure your property for its rebuild cost — not its market value.

The rebuild cost is what it would cost to completely demolish and rebuild your home from scratch, including materials, labour, and professional fees such as architects and surveyors. This is almost always lower than what you paid for the property, because the market value includes the land, which cannot be destroyed in a fire.

If you insure your home for less than the true rebuild cost, you could find yourself underinsured. This means that in the event of a major claim, the insurer may only pay out a proportion of the cost. Equally, over-insuring means you are paying unnecessarily high premiums for cover you do not need.

The best way to get an accurate rebuild cost figure is to use the Royal Institution of Chartered Surveyors (RICS) rebuild calculator — marked here in red as an outbound reference — or to commission a professional building survey. Many insurers will also provide guidance during the quote process, but it is worth doing your own research first.

Not sure what cover you need for your property?

Understanding your legal obligations as a homeowner, especially when a mortgage is involved, can be confusing. If you are currently going through a property purchase and want to know where you stand, contact our conveyancing team at Versus Law — we can help you understand exactly what your mortgage lender requires before completion.

Do I need contents insurance as well?

Buildings insurance protects the structure of your home, but it does not cover the things inside it. That is where contents insurance comes in. Contents insurance covers your personal belongings — furniture, electronics, clothing, jewellery, appliances, and other household items — against risks like fire, theft, flood, and accidental damage.

If you rent your home, you do not need buildings insurance — that is the landlord’s responsibility. However, contents insurance is strongly recommended for renters, as it protects the belongings you have brought into the property.

What does contents insurance cover?

A standard contents insurance policy covers your belongings against damage or loss caused by fire, flooding, theft, and storm damage. You can often add accidental damage cover as an optional extra, which is useful if you have children or pets.

When taking out contents insurance, you need to work out the total value of everything you own inside the home. This includes:

- Furniture and soft furnishings

- White goods such as washing machines and fridges

- Electronics including televisions, laptops, and smartphones

- Clothing and footwear

- Jewellery and watches

- Artwork, antiques, or collections

Be aware that most policies have a single-item limit, which caps the amount they will pay out for any one item. If you own expensive jewellery or high-value electronics, you may need to list those items separately or take out specialist cover. Underestimating the value of your contents means you could be left short if you ever need to make a claim.

Buildings and contents insurance — should you combine them?

Many insurers offer combined home insurance policies that bundle buildings and contents cover together. This can be more convenient than managing two separate policies and is often more cost-effective. If you are a homeowner rather than a renter, a combined policy is usually the most straightforward option.

When comparing quotes, always check what is included and excluded in each policy rather than simply choosing the cheapest option. A policy that does not cover flooding, for example, could be a serious problem if your property is in a high-risk area.

Other factors that affect the cost of home insurance include your postcode, the age and construction of your property, the security measures you have in place, and your claims history. Installing approved locks and a monitored alarm system can often reduce your premium.

What do mortgage lenders require?

If you are buying a property with a mortgage, your lender will require you to have buildings insurance in place from the date of exchange of contracts — not just completion. This is because from exchange onwards, the legal risk for the property passes to the buyer. If something happened to the building between exchange and completion, you would be liable.

Most mortgage lenders will ask to see proof of buildings insurance before they release the mortgage funds. Some lenders have their own approved insurers, though you are not legally obliged to use them. You are free to shop around and choose a policy that suits you, provided it meets the lender’s minimum requirements.

If you are buying a leasehold property — such as a flat — the freeholder or management company will usually arrange buildings insurance for the whole building and pass the cost on to leaseholders through the service charge. In this case, you would not need to arrange your own buildings insurance, but contents insurance would still be your responsibility.

Our residential conveyancing team regularly advises buyers on their obligations at each stage of a property transaction, including what insurance you need and when.

Tips for getting the right home insurance policy

Getting the right cover does not have to be complicated. Here are some straightforward steps to help you find a policy that works for you:

- Use the rebuild cost — not the market value — as your buildings sum insured

- Add up the realistic replacement value of all your contents before getting a quote

- Check whether the policy covers flood risk if your property is in a vulnerable area

- Consider combining buildings and contents insurance with one insurer for simplicity and potential savings

- Review your policy annually rather than auto-renewing, as premiums often increase at renewal

- Improve your home security to qualify for lower premiums

If you are in the process of buying a home, it is also worth speaking with your conveyancing solicitor about your insurance obligations. Knowing exactly when your cover needs to start — and what it needs to include — can save you from expensive surprises later on. Our conveyancing solicitors in Manchester are experienced in guiding buyers through the full property purchase process.

Ready to move forward with your property purchase?

Whether you are a first-time buyer or moving up the property ladder, having the right home insurance in place is a key part of a smooth transaction. Our experienced conveyancing team at Versus Law can help you understand your obligations, meet your mortgage lender’s requirements, and complete your purchase with confidence.

-

Gazumping and gazundering explained: what every UK buyer and seller needs to know

-

Why do people avoid leasehold properties?

-

Estate agent fees explained: what UK sellers really pay

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

Estate agent fees explained: what UK sellers really pay

Estate agent fees are one of the first costs people think about when selling their home. Yet despite being so common, they remain widely misunderstood. How much do estate agents charge? What does the fee actually cover? And can you negotiate it down?

This guide answers all of that in plain English. Whether you’re selling for the first time or just want to know if you’re getting a fair deal, you’ll find everything you need right here.

How much do estate agents charge in the UK?

On average, estate agent fees in the UK sit at around 1% to 1.8% of the sale price (including VAT) for a sole agency agreement. That means one agent has the exclusive right to sell your property during the agreed period.

To put that into real numbers: if your home sells for £300,000 and you agree a fee of 1.5%, you’d pay £4,500. On a £500,000 property at the same rate, the fee would be £7,500.

Of course, fees can fall outside this typical range. Here’s a rough breakdown by arrangement type:

- Sole agency: typically 1% to 1.8%, sometimes up to 2.5%

- Multi-agency: usually 2.5% to 3.6% — higher because multiple agents compete, but you only pay the one who finds your buyer

- Online/fixed-fee agents: often £300 to £1,500 as a fixed charge, sometimes paid upfront

- No sale, no fee: built into most traditional agent agreements; you pay nothing if the sale falls through

These are averages and starting points. The actual fee you pay depends on the agent, your location, your property type, and — importantly — what you negotiate.

What’s included in estate agent fees?

Most estate agent fees cover a standard package of services. When comparing agents, it helps to know what you should reasonably expect at no extra charge:

- A free property valuation

- Listing on major property portals such as Rightmove and Zoopla

- Professional photography and a written property description

- Arranging and conducting viewings

- Receiving and presenting offers to you

- Negotiating with buyers on your behalf

- Progressing the sale from accepted offer through to completion

Some agents charge separately for floor plans, premium portal listings, For Sale boards, or Energy Performance Certificates. Always ask what’s included before you sign anything.

Types of estate agent agreements

The type of agreement you sign has a direct impact on how much you pay and what you’re committed to. There are three main options:

Sole agency

This is the most common arrangement. You appoint a single agent to sell your property, and they earn their fee only if they find your buyer. If you find a buyer independently (for example, a neighbour who expresses interest), you generally don’t owe the agent anything.

Sole agency fees tend to be the lowest, and this arrangement is usually the best starting point for most sellers.

Sole selling rights

Similar to sole agency, but with one important difference: the agent is paid even if you find the buyer yourself. This type of agreement is less common and generally best avoided unless you have a specific reason to agree to it.

Multi-agency

You appoint several agents at once, all of whom can market your property. You only pay the one who successfully sells it — but the fee will be higher to reflect the risk agents take on by competing without a guarantee.

Multi-agency can be worth considering if your property is proving difficult to sell or if you want to generate more competition among agents quickly.

Not sure what you’ll owe beyond the agent’s fee?

Selling your home involves more than just the estate agent’s commission. Solicitor costs, conveyancing fees, and other legal charges also need to be factored in. Get in touch with our conveyancing team and we can walk you through the full picture before you commit to anything.

When and how estate agent fees are paid

In most cases, you don’t pay the estate agent directly out of your pocket on the day of sale. Your solicitor will typically deduct the agent’s fee from the sale proceeds before transferring the remaining funds to you.

This is one reason why it pays to have a reliable conveyancing solicitor on your side. If you’re not sure what conveyancing fees typically involve, it’s worth getting a clear breakdown upfront so you’re not caught off guard.

Most agreements state that fees are due on completion — the day ownership of the property legally transfers to the buyer. However, some contracts specify that fees become due at exchange of contracts, which is an earlier stage. Read your agreement carefully, particularly if there’s any risk of the sale falling through at a late stage.

For fixed-fee online agents, payment is often required upfront — meaning you could lose the fee if the property doesn’t sell. Always check the payment terms before instructing any agent.

Can you negotiate estate agent fees?

Yes — and in many cases, you should. Estate agents expect buyers to negotiate, especially on higher-value properties where even a small reduction in percentage terms can save a significant amount of money.

A few things that can strengthen your negotiating position:

- Your property type and price: agents are often more flexible on higher-value homes where their total commission is larger

- Market conditions: in a strong seller’s market, agents may reduce their fee more readily to win your instruction

- Multiple quotes: getting three or more valuations gives you real data to negotiate with — not just a feeling

- Longer contracts: some agents will reduce their fee in exchange for a longer exclusive period

Don’t just negotiate the percentage — also ask about the notice period to withdraw from the agreement, and whether you can switch to multi-agency if the property hasn’t sold within a set timeframe.

Online estate agents vs high street agents

One of the biggest decisions when selling your home is whether to go with an online agent or a traditional high street agency. Both have genuine advantages depending on your situation.

Online agents typically charge fixed fees ranging from a few hundred pounds up to around £1,500. The appeal is clear: you could save thousands compared with a percentage-based fee. However, these packages often require more involvement from you — particularly when it comes to conducting viewings or chasing the sale through.

High street agents charge more, but they usually provide a more hands-on service. An experienced local agent can draw on knowledge of your area’s market, negotiate actively with buyers, and keep the sale moving if complications arise.

The cheapest option isn’t always the best value. An agent who achieves a significantly higher sale price, even at a higher fee, can leave you better off overall. Understanding the full conveyancing process from accepted offer to completion can help you see why having experienced professionals in your corner — on both the legal and sales side — matters.

Tips for choosing the right estate agent when selling your home

With so many agents competing for your instruction, it can be hard to know where to start. Here are some practical tips to help you make the right choice:

- Get at least three valuations: this helps you spot outliers — both agents who overvalue to win your business and those who undervalue to secure a quick sale

- Ask for comparable evidence: a good agent should be able to show you recent sold prices for similar properties in your area, not just an educated guess

- Check their track record: look at online reviews, sold listings, and how quickly they typically move properties in your price range

- Read the contract carefully: pay attention to the tie-in period, the definition of ‘introduced buyer’, and what happens if you find your own buyer

- Think about the full cost of selling: estate agent fees are just one part of the picture — legal and conveyancing fees also need to be budgeted for

According to The Property Ombudsman, sellers have the right to clear, upfront information about all fees and terms before signing any agency agreement. If an agent is vague or evasive about costs, that’s a warning sign worth heeding.

Is VAT included in estate agent fees?

Not always — and this is a detail that catches many sellers off guard. When an agent quotes you a percentage fee, always ask whether that figure includes VAT.

VAT is currently charged at 20% in the UK. So a quoted fee of 1.5% excluding VAT actually becomes 1.8% once VAT is added. On a £300,000 property, that’s the difference between paying £4,500 and paying £5,400.

Reputable agents should be transparent about this from the outset. Always confirm in writing whether any quoted figure is inclusive or exclusive of VAT before you proceed.

Ready to take the next step with selling your home?

Once you’ve chosen your estate agent, the legal side of your sale begins. Our specialist conveyancing solicitors can help you understand your full costs, deal with the paperwork, and keep your sale on track from accepted offer through to completion.

Get in touch today — or use our instant calculator to see what your conveyancing fees might look like.

-

Gazumping and gazundering explained: what every UK buyer and seller needs to know

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

What is joint tenancy vs tenants in common?

When buying a property with someone else, one of the most important decisions you’ll make is how to legally own it together. The choice between joint tenancy vs tenants in common affects what happens to your share if you die, what happens if the relationship breaks down, and how the proceeds of a future sale are divided.

This guide explains both options in plain English so you can make an informed decision — whether you’re buying with a partner, a friend, a family member, or a business associate.

What is joint tenancy?

Joint tenancy is a form of shared ownership where two or more people own a property together as a single, unified entity. Each owner has equal rights to the whole property — there are no individual shares or percentages. It does not matter if one person paid a larger deposit or contributes more to the mortgage; legally, all joint tenants own the property equally.

The most significant feature of joint tenancy is the right of survivorship. This means that when one owner dies, their interest in the property automatically passes to the surviving owner — regardless of what their will says, and without needing to go through probate.

For married couples or civil partners buying together, joint tenancy is a common and often sensible default. It provides automatic protection for the surviving partner, is straightforward to administer, and avoids the need for specific provisions in a will relating to the property.

What joint tenancy means in practice

- You own the whole property together — not a specific “share”

- All owners must agree before the property can be sold

- If one owner dies, the property passes automatically to the survivor

- You cannot leave your interest in the property to someone else in your will

- Proceeds from a sale are always split equally

What is tenants in common?

Tenancy in common is a form of shared ownership where each person holds a distinct, separate share of the property. Those shares can be equal — such as 50/50 — or unequal, for example 70/30 or 60/40. This arrangement is particularly useful when buyers are contributing different amounts to the deposit or purchase price.

Unlike joint tenancy, there is no right of survivorship in tenants in common. When one owner dies, their share does not automatically pass to the other owner. Instead, it passes according to their will — or, if they do not have a will, according to the intestacy rules. This means the surviving owner may find that they now co-own the property with the deceased’s family members, children from a previous relationship, or even a stranger.

Tenants in common gives each owner much more flexibility and control over their individual share. Each person can — in principle — sell or mortgage their own share independently, and can choose who inherits it. However, this flexibility also introduces complexity, which is why having a declaration of trust is strongly recommended.

What tenants in common means in practice

- Each owner holds a defined share, which can be equal or unequal

- You can specify who inherits your share through your will

- No right of survivorship — your share does not automatically pass to the other owner

- A declaration of trust should be drawn up to record the shares and agree how proceeds are split

- Particularly useful when buyers contribute unequal amounts, or have children from previous relationships to consider

The right of survivorship: what it means and why it matters

The right of survivorship is the legal rule that applies automatically to joint tenants. When one owner dies, their interest in the property transfers immediately and in full to the surviving owner — bypassing the will, bypassing probate, and bypassing any claims from family members.

This can be enormously valuable for couples. If one partner dies unexpectedly, the other retains full ownership and control of the family home without any legal uncertainty. For unmarried couples in particular, this is significant — because without the right of survivorship, there is a real risk that the deceased’s share could end up in the hands of their family rather than their partner.

However, the right of survivorship is also a limitation. If you own as joint tenants and want your share to pass to your children from a previous relationship, or to a sibling, or to anyone other than your co-owner — you cannot do that within a joint tenancy. This is often the main reason couples or co-buyers choose tenants in common instead.

Consider this example: two people own a property together as joint tenants. One dies and their share automatically passes to the survivor. The survivor then remarries and eventually leaves the entire property to their new spouse. The original deceased’s children receive nothing. Had the property been held as tenants in common, the deceased could have directed their share to their own children in their will.

Declaration of trust: what it is and when you need one

A declaration of trust (sometimes called a deed of trust or trust deed) is a legally binding document that records the ownership arrangement between co-owners. It sets out each person’s share, how the property was funded, and what should happen in various circumstances — such as one person wanting to sell, or the relationship breaking down.

If you are buying as tenants in common, a declaration of trust is not legally required — but it is strongly recommended. Without one, the law assumes ownership is split 50/50, regardless of who paid what. If one person contributed 70% of the deposit and there is no deed in place, they may struggle to prove their greater financial contribution if a dispute arises later.

A well-drafted declaration of trust should cover:

- The percentage share each owner holds

- What each person contributed to the deposit and purchase price

- How ongoing mortgage payments and costs are allocated

- What happens if one person wants to sell but the other does not

- How sale proceeds are distributed when the property is eventually sold

For joint tenants, a declaration of trust is less commonly used — since there are no separate shares to record — but it can still be useful to document financial arrangements between co-owners.

Joint tenancy decisions are made as part of the wider conveyancing process, and your solicitor will guide you through the right option for your situation before you register the property.

Not sure how to own a property with someone else?

Joint tenancy and tenants in common give you very different rights over ownership, inheritance, and sale. Get expert advice before you commit.

Which is right for you: joint tenancy or tenants in common?

There is no single correct answer to the question of joint tenancy vs tenants in common. The right choice depends on your circumstances, your relationship with your co-owner, your financial contributions, and your plans for the future.

Joint tenancy may be the better choice if:

- You are married or in a civil partnership and want ownership to pass automatically to your partner

- You both have equal financial contributions and want a simple, unified ownership structure

- You want to avoid the need for specific property provisions in your will

- You are buying in a committed relationship and want equal security for both of you

Tenants in common may be the better choice if:

- You and your co-owner are contributing different amounts and want ownership to reflect that

- You have children from a previous relationship and want to protect their inheritance

- You are buying with a friend, sibling, or business associate rather than a romantic partner

- You want the freedom to leave your share to whoever you choose in your will

- You are concerned about care home fees — tenants in common can help protect part of the property from local authority assessment

What happens if you want to change ownership type?

It is possible to change from joint tenancy to tenants in common — or from tenants in common to joint tenancy — after you have already registered the property. This is done through a legal process called severance of joint tenancy (to convert from joint to tenants in common) or by executing a new deed of trust (to convert from tenants in common to joint).

Circumstances that often prompt a change include:

- Separation or divorce — where one partner wants to be able to leave their share to someone other than their ex

- Marriage or entering a civil partnership — where a couple want to switch to joint tenancy for automatic survivorship

- Change in financial circumstances — where one person has contributed significantly more over time

- Estate planning — where a couple want to protect their respective shares for inheritance tax or care cost purposes

You can notify HM Land Registry directly of a change in ownership type by submitting a form — this is free to do. However, if you want to record the specific shares held and set out the terms of the arrangement, a solicitor should prepare the formal documentation. The GOV.UK guidance on joint property ownership sets out the forms and process involved if you wish to manage this yourself.

Inheritance tax considerations

Both forms of joint ownership can have inheritance tax implications, though the detail depends on the relationship between the owners and who inherits.

When one joint tenant or tenant in common dies and the property passes to their spouse or civil partner, no inheritance tax is due on that transfer — regardless of the ownership type. The spousal exemption applies in both cases.

Where the property passes to someone other than a spouse or civil partner, the value of the deceased’s share is added to the total estate for inheritance tax purposes. This is the same whether you hold as joint tenants or tenants in common — the difference is in who receives the share, not whether tax is due. Careful estate planning, including making a will, is important for anyone co-owning property outside of a marriage or civil partnership.

Summary

The choice between joint tenancy vs tenants in common is one of the most consequential decisions you will make when buying a property with someone else. It determines what happens when one of you dies, what happens if you separate, and how any future sale proceeds are divided.

Joint tenancy is simple, equal, and provides automatic protection for the surviving owner through the right of survivorship. Tenants in common offers more flexibility — particularly around inheritance — but requires more careful planning, ideally including a declaration of trust and an up-to-date will.

Both options form part of the conveyancing process, and your solicitor will advise you on which is appropriate for your circumstances. If you are unfamiliar with what conveyancing involves, our guide to what conveyancing solicitors actually do explains the role of legal support in any property transaction.

If you are about to buy a property and want to understand the full legal process — including how ownership type is registered and what documentation is required — our guide to the stages of the conveyancing process covers everything from initial instruction to completion. Alternatively, if you have a specific question about your situation, our conveyancing team is happy to help.

Need advice on joint tenancy vs tenants in common?

The way you own a property affects what happens if one owner dies, how sale proceeds are divided, and whether you can leave your share to someone else. Choosing between joint tenancy and tenants in common should reflect your relationship, financial contributions, and long-term plans. Our solicitors can guide you through the options and help you structure ownership correctly from the outset.

-

Gazumping and gazundering explained: what every UK buyer and seller needs to know

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

Estate agent fees explained: what UK sellers really pay

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

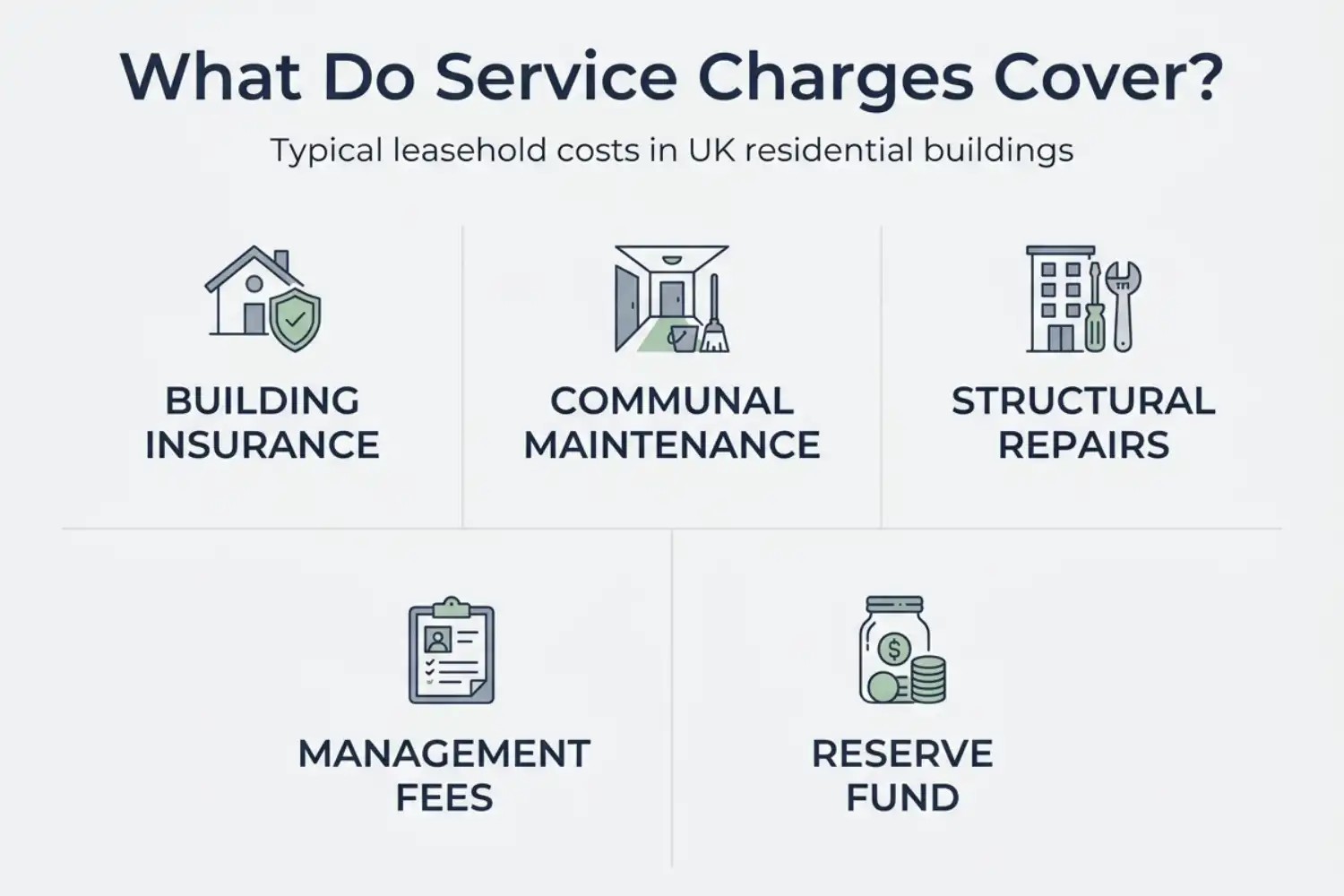

What are service charges and what do they cover?

Service charges are one of the most significant ongoing costs for leasehold property owners in the UK — and one of the least well understood before purchase. At their core, service charges leasehold arrangements require flat owners and long leaseholders to contribute to the costs of maintaining and managing the building they live in. But what those charges actually cover, how they are calculated, and what your rights are when they seem unreasonable are questions that trip up buyers and existing owners alike.

This guide explains what service charges are, what do service charges cover in practice, how the figures are set, and what protections the law gives you as a leaseholder. Understanding leasehold property costs at this level of detail matters particularly before you buy — because service charges that look manageable today can change significantly, and buyers who do not ask the right questions before exchange can face surprises that affect both their budget and their resale value.

What are service charges in leasehold properties?

A service charge is a payment made by a leaseholder to the landlord, freeholder, or managing agent to cover the costs of services provided to the building and its shared areas. The legal basis for the charge comes from the lease itself — the landlord can only recover costs through a service charge if the lease expressly provides for it. If the lease does not include a particular cost, the landlord cannot charge for it regardless of what work was carried out.

Service charges are distinct from ground rent, which is a payment made simply for the right to occupy the land under the property and does not relate to services provided. For most new leases granted after 30 June 2022, ground rent is capped at a peppercorn (effectively zero), but service charges remain a live and variable leasehold property cost throughout the entire term of the lease.

The amount payable as service charges leasehold owners face is not fixed in advance indefinitely. In most residential leases, service charges are variable — meaning they change year on year depending on what has actually been spent on the building. The lease will specify how each leaseholder’s share is calculated: it may be expressed as a percentage of total costs, as a proportion based on floor area, or simply as a “fair and reasonable proportion.” Whatever the formula, each leaseholder pays a defined share of the building’s total outgoings.

What do service charges cover?

The specific items covered by a service charge depend on the lease, the type of property, and what the freeholder or managing agent has contracted to provide. However, the categories that commonly appear across residential leasehold buildings in the UK include the following.

Building insurance

Your landlord is usually responsible for insuring the fabric of the building — the structure, roof, and common parts — and the cost of that insurance premium is recovered through the service charges leasehold arrangement. This covers the building itself; it does not cover your personal possessions or contents, for which you need separate cover. Before purchasing a leasehold property, it is worth checking both the level of building insurance in place and how the premium has changed over recent years, as significant increases will be reflected in your service charge.

Maintenance and repair of communal areas

The day-to-day upkeep of everything outside your front door but within the building is typically covered by the service charge. This is one of the more predictable categories of leasehold property cost and includes:

- Cleaning of hallways, stairwells, lobbies, and communal corridors

- Lighting of shared spaces and external areas

- Lift maintenance, servicing, and repair

- Maintenance of entry systems, intercoms, and communal doors

- Window cleaning on communal and external glazing

- Upkeep of any shared garden areas, car parks, or external paths

Repairs and maintenance of the building structure

The exterior fabric of the building — the roof, foundations, guttering, communal drains, and external walls — generally falls within what service charges cover for the freeholder to maintain. In an FRI (Full Repairing and Insuring) arrangement, these costs are passed directly to leaseholders through the service charge. The extent to which structural repairs are the landlord’s responsibility rather than the tenant’s depends on how the lease is drafted.

Management fees

Where a professional managing agent is appointed to run the building — collecting service charges, arranging maintenance contracts, dealing with insurance, and managing the building’s day-to-day affairs — their fees are recovered through the service charges leasehold residents pay. Management fees vary considerably depending on the size and complexity of the building, and they are a legitimate cost that can be included in the service charge provided they are reasonable. Leaseholders have the right to challenge management fees they consider disproportionate.

Reserve fund and sinking fund

Most well-managed buildings include a contribution to a reserve fund — sometimes called a sinking fund — within the annual service charge. This is money set aside against the cost of future major works, such as replacing the roof, refurbishing the communal areas, or overhauling the lifts. The purpose is to spread the cost of large-scale repairs across all leaseholders and across time, so that no single year’s service charge is disproportionately high.

Understanding what do service charges cover in this context is particularly important at the point of purchase. A building with a healthy sinking fund is likely to have more predictable future costs than one where no reserve has been built up — because the latter will either defer necessary maintenance (creating problems later) or hit leaseholders with a large, unplanned bill when the work can no longer be put off.

How service charges leasehold owners pay are calculated

Service charges in residential leasehold properties typically operate on an advance estimate basis. At the beginning of each service charge year, the landlord or managing agent issues an estimated budget for the year ahead. Leaseholders pay instalments based on this estimate — usually monthly, quarterly, or annually — throughout the year.

At the end of the year, the actual expenditure is reconciled against the estimate. If the building spent more than anticipated, leaseholders are asked to make up the shortfall. If it spent less, the surplus is either credited to the following year’s account or, in some cases, refunded. This means your service charge in any given year is not entirely predictable in advance — it is adjusted once actual costs are known.

The share of the total cost you pay as an individual leaseholder is set out in your lease. Common methods include a percentage allocation to each unit (which may or may not reflect floor area), an equal split between all flats, or a proportionate split based on the size or type of each unit. Some leases specify that each leaseholder pays a “fair and just proportion,” which gives less certainty but allows for flexibility where properties are substantially different in size.

What service charges cover can also vary between buildings in the same development. In large mixed-use schemes, the service charge structure can be complex, with different buildings or phases contributing to different service charge pools depending on which facilities they have access to.

Major works and Section 20 consultation

One of the most significant financial events in any leaseholder’s experience is a major works programme — a large-scale project affecting the building, such as roof replacement, external redecoration, or lift overhaul. These projects can cost tens or hundreds of thousands of pounds in total, with each leaseholder’s share potentially running into thousands.

The law provides important protections at this point. Under Section 20 of the Landlord and Tenant Act 1985, a landlord who proposes to carry out works that will cost any individual leaseholder more than £250, or to enter into a long-term maintenance contract that will cost any leaseholder more than £100 per year, is required to carry out a formal consultation process before committing to that expenditure. This Section 20 process involves notifying leaseholders of the proposed works, inviting them to nominate contractors for consideration, and giving them the opportunity to comment on the estimates obtained.

If the landlord does not comply with the Section 20 consultation requirements, their ability to recover costs from leaseholders is capped at £250 per leaseholder for the works in question. This is a meaningful protection — it means that skipping or shortcutting the consultation process has a direct financial consequence for the landlord. As a leaseholder facing major works, knowing whether the Section 20 process has been properly followed is one of the most important things to check before agreeing to pay.

Not sure what service charges really cover?

Service charges can include insurance, maintenance, management fees and future repair costs — and they can change over time. Get expert advice before committing to a leasehold property.

Your rights as a leaseholder in relation to service charges

The right to information

Leaseholders have a statutory right to request a written summary of the costs incurred during the previous accounting year, showing how the service charge has been calculated and what the funds were spent on. You can also request access to the supporting invoices, receipts, and contracts. The landlord must comply with this request within a reasonable time. Understanding what do service charges cover in your specific building — as opposed to in general — requires this level of transparency, and you are entitled to it.

The right to challenge

Service charges leasehold owners pay are only recoverable by the landlord if they are reasonable. If you believe a charge is unreasonable — whether because the work was unnecessary, the cost was excessive, or the service was not actually provided — you have the right to apply to the First-tier Tribunal (Property Chamber) to have the charge assessed. The Tribunal can determine whether the costs are reasonable and, if not, reduce them. You cannot apply to the Tribunal in respect of a fixed service charge (one whose amount is set in the lease itself), but variable charges — which are the norm in residential leasehold — are challengeable.

Challenging a service charge is a serious step that should be considered carefully, ideally with legal advice. However, the right to do so is an important protection given the scale of leasehold property costs and the potential for mismanagement or overcharging. The Leasehold Advisory Service (LEASE) is a free government-funded service that provides guidance to leaseholders navigating disputes with their landlord or managing agent.

Protection of service charge funds

Service charge contributions must be held on trust by the landlord, in a separate account designated for that purpose. This means that if the landlord or managing agent becomes insolvent, the service charge funds are protected and cannot be claimed by their creditors. It is a basic but important protection that ensures the money you have paid for building maintenance cannot be lost in the event of a freeholder’s financial failure.

What do service charges cover when you are buying a leasehold property?

For buyers of leasehold properties, service charges leasehold arrangements represent a recurring cost that needs to be factored into affordability from the outset. The conveyancing process is the point at which you should gather the detailed information needed to understand what those charges look like — both historically and going forward.

During the purchase process, your solicitor will request the management information pack for the property. This includes three years of service charge accounts showing what has been spent and how the charges have been apportioned, any outstanding service charge balances the seller may owe, the current year’s estimated budget, and details of any planned major works. Reviewing this information carefully gives you a realistic picture of your likely leasehold property costs in the coming years and allows you to identify any red flags — such as an underfunded sinking fund, an upcoming major works programme, or a pattern of rapidly rising annual charges. Understanding the leasehold financial structure, including the LPE1 form that formalises this information transfer between seller and buyer, is covered in detail in our guide to what the LPE1 form is and why it matters in leasehold transactions.

If you want to understand the full financial picture of buying a leasehold property — including how service charges affect the conveyancing fee calculation — our instant conveyancing cost calculator gives you a transparent breakdown of all costs involved in your specific purchase, including the additional leasehold fee.

Getting proper advice on service charges leasehold properties

Service charges are one of the most important financial considerations in any leasehold property purchase or ownership, and they are an area where independent legal advice makes a material difference. A conveyancing solicitor reviewing your purchase will examine the service charge history, identify any outstanding balances or planned works, and advise you on what the figures mean for your leasehold property costs in the years ahead. They will also flag any concerns about the management of the building that could affect your ability to sell or remortgage in the future. Our residential conveyancing team advises buyers, sellers, and existing leaseholders across England and Wales on all aspects of leasehold transactions, including service charge reviews and disputes. If you have a question about your service charges or are in the process of buying or selling a leasehold property, get in touch with our team for a straightforward, no-obligation conversation about your situation.

Need advice on leasehold service charges before you buy?

Service charges are one of the biggest ongoing costs of leasehold ownership, and they are not always predictable. Understanding what they cover, how they are calculated, and whether major works are planned is essential before you commit. Our solicitors review service charge accounts, explain the risks, and help you make an informed decision before exchange.

-

Gazumping and gazundering explained: what every UK buyer and seller needs to know

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

Estate agent fees explained: what UK sellers really pay

-

What is joint tenancy vs tenants in common?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house

OTHER NEWS

What happens if a conveyancing search reveals a problem?

Discovering a conveyancing search problem during the process of buying a house is more common than most buyers expect — and it is rarely the end of the road. Searches are designed to surface exactly these issues before contracts are exchanged, which means finding a problem at this stage is actually the system working as it should.

What matters most when property search results flag something unexpected is understanding what your options are and acting on the right advice quickly. A conveyancing search problem can lead to renegotiation, specialist investigation, indemnity insurance, or — in the most serious cases — withdrawal from the purchase. This guide walks through each type of problem, what triggers it, and what you can realistically do about it.

What conveyancing searches actually check

Before exploring what happens when something goes wrong, it helps to understand what conveyancing searches are looking for. When you are buying a house, conveyancing searches are a set of formal enquiries made to various public bodies and registries to gather information that would not be apparent from a viewing, a survey, or even the Land Registry title documents alone.

The core searches that produce property search results in most residential transactions are:

- Local authority search: checks planning permissions, building regulation decisions, enforcement notices, road adoption status, tree preservation orders, conservation area designations, and listed building status.

- Water and drainage search: confirms how the property connects to public sewers and water mains, identifies the location of shared drains and pipes, and flags any history of sewer flooding.

- Environmental search: assesses flood risk, contaminated land, proximity to landfill sites, radon gas levels, ground stability issues, and other environmental hazards.

- Land Registry search: confirms ownership, identifies any restrictions, covenants, or easements registered against the title.

Additional searches may be ordered depending on the property’s location and history. In former mining areas — parts of Cornwall, South Wales, the Midlands, and the North of England — a mining search is standard. In some areas, a chancel repair search is also advisable to check whether the property carries an ancient obligation to contribute to Church of England repair costs. Your solicitor will advise which searches are appropriate for the specific property you are buying. If a conveyancing search problem emerges from any of these checks, the nature and severity of the issue determines what happens next.

The most common conveyancing search problems

Not all issues flagged by searches are equally serious. Some are informational — confirming something the seller already mentioned, or showing a planning consent that has already been complied with. Others are more significant and require careful consideration before you proceed with buying a house. The most common problems that emerge from searches include:

Planning and building regulation issues