What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

Property auction fees can add significantly more to your total purchase cost than most first-time bidders expect. Beyond the hammer price, there are multiple charges — some fixed, some percentage-based, some hidden in the legal pack — that can easily run to thousands of pounds.

This guide breaks down every fee you are likely to encounter when buying at property auction in the UK, so you can budget accurately before you raise your paddle and avoid any costly surprises after the hammer falls.

Why property auction fees catch buyers off guard

Most buyers focus on the hammer price — the amount they bid — as the total cost of their purchase. In reality, that figure is just the starting point. Property auction fees layer on top of it, and if you have not factored them into your budget in advance, you can find yourself in a difficult position very quickly.

The situation is made more urgent by the nature of auction contracts. The moment the hammer falls, you are legally committed to completing the purchase. There is no cooling-off period, no time to reassess your finances, and no opportunity to renegotiate once you have won the bid.

This is why experienced buyers always calculate their total acquisition cost — including all auction conveyancing costs — before placing a single bid. Understanding the full picture before auction day is not just sensible; in most cases, it is the difference between a profitable purchase and a serious financial loss.

The buyer’s premium: what it is and how much it costs

The buyer’s premium is an additional fee charged by the auction house on top of the hammer price. It is effectively the auction house’s commission for facilitating the sale, and it is almost always payable by the buyer rather than the seller.

The amount varies between auction houses, but typical buyer’s premiums in the UK range from 1% to 5% of the hammer price, plus VAT. On a £200,000 property, that means anywhere from £2,400 to £12,000 in additional cost before you have even considered legal fees, stamp duty, or surveys.

Some auction houses charge a fixed buyer’s premium rather than a percentage — commonly between £1,500 and £5,000 plus VAT — regardless of the hammer price. Others use a tiered structure where the percentage decreases as the purchase price rises. Always read the auction house’s terms of business carefully before the auction, as the buyer’s premium is non-negotiable and must be paid on the day along with your deposit.

The deposit: how much you need on the day

When your bid is accepted at a traditional unconditional auction, you will be required to pay a deposit immediately. This is typically 10% of the hammer price, though some auction houses set a minimum — for example, requiring at least £5,000 regardless of the purchase price.

The deposit is paid directly to the auctioneer on the day, usually by cheque or bank transfer. You cannot pay by credit card, and you cannot delay payment — the deposit and the buyer’s premium are both payable before you leave the auction room (or on the same day if bidding online).

If you fail to complete the purchase within the required timeframe — usually 28 days for a traditional auction — the seller is entitled to keep your entire deposit. This risk underlines why auction buyers must have their financing firmly in place before they bid, not after.

Many buyers use short-term finance to fund auction purchases within the tight completion window. Understanding bridging finance for auction purchases is essential if you cannot complete with cash or a mortgage arranged in advance.

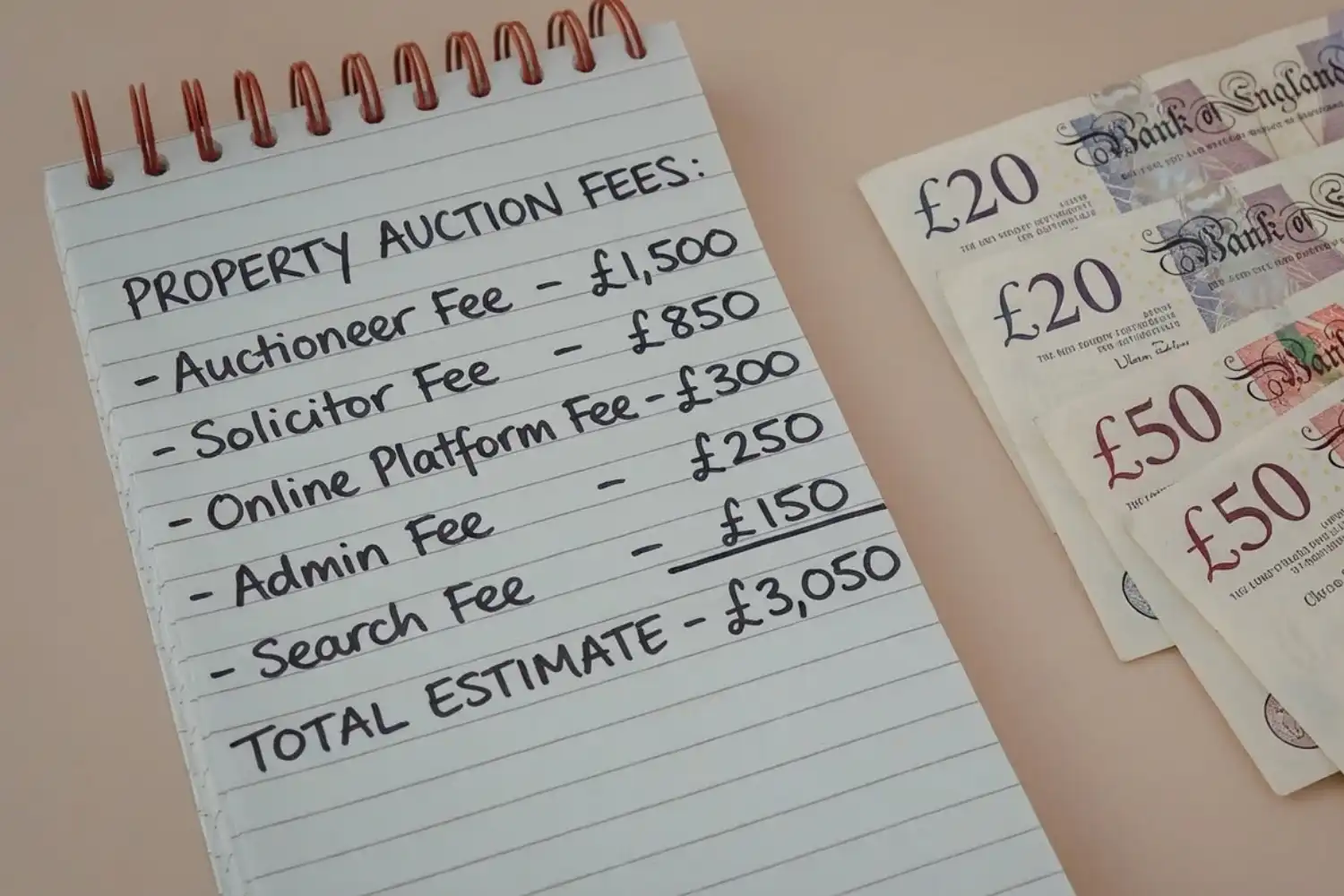

Auction conveyancing costs: what solicitors charge for auction work

Conveyancing at auction is faster and more complex than a standard property purchase, and the legal fees reflect this. You will need a solicitor both before and after the auction — before to review the legal pack, and after to complete the transaction within the required timeframe.

Pre-auction legal pack review

Before you bid, you should have a solicitor review the auction legal pack. This is a set of documents provided by the seller’s solicitor — including the title register, special conditions of sale, searches, and any planning or tenancy information. Many auction properties have legal issues buried in the pack that can affect their value, mortgageability, or future saleability. A pre-auction legal review typically costs £150 to £400 plus VAT, and can save you from winning a bid on a property you should never have bought.

One area that deserves particular attention is the Special Conditions of Sale. These can require the buyer to pay the seller’s legal fees, stamp duty contributions, or administration charges that are not immediately obvious from the guide price. Experienced auction conveyancing solicitors will identify these obligations and calculate the true cost of the purchase before you commit.

Post-auction conveyancing fees

Once you have won the bid, your solicitor will manage the full conveyancing process to completion — typically within 28 days. Because of the compressed timeline, auction conveyancing fees tend to be higher than those for a standard property purchase.

Typical post-auction conveyancing costs in the UK range from £800 to £1,800 plus VAT and disbursements for a residential purchase, though this varies by property value and complexity. Fixed-fee conveyancing services are available and can offer more predictable costs for auction buyers.

Stamp duty land tax: a major property auction fee many buyers underestimate

Stamp duty land tax (SDLT) is charged on most property purchases in England and Northern Ireland above certain thresholds. It is not an auction-specific fee — it applies to all property purchases — but it is one of the largest costs involved in buying at property auction, and one that first-time buyers in particular can underestimate.

Current SDLT rates for residential purchases in England are:

- 0% on the first £125,000 of the purchase price

- 2% on the portion from £125,001 to £250,000

- 5% on the portion from £250,001 to £925,000

- 10% on the portion from £925,001 to £1.5 million

- 12% on the portion above £1.5 million

An additional 3% surcharge applies if you already own another property. First-time buyers benefit from relief on properties up to £500,000. You can check the exact figure for your purchase using the government’s SDLT calculator.

Stamp duty must be paid within 14 days of completion. On a £300,000 property purchased as an additional property, you could face an SDLT bill of around £17,000 — a significant sum that needs to be factored into your pre-auction budget.

Land Registry fees

Every property purchase in England and Wales must be registered with HM Land Registry, and a fee is payable to do so. The amount depends on the value of the property and whether the application is submitted electronically or by post.

For a £200,000 residential purchase submitted electronically, the Land Registry fee is £270. For a £500,000 purchase, it rises to £540. These are fixed fees set by the government and are not negotiable. Your solicitor will pay this on your behalf as a disbursement and include it in your completion statement.

Unsure what you will actually pay on top of the winning bid?

Auction buyers often budget for the purchase price but overlook extra costs hidden in the

legal pack or sale conditions. A clearer breakdown of auction fees can help you set a safer

maximum bid and avoid expensive surprises after the auction ends.

See how a solicitor helps protect auction buyers from costly mistakes

Survey costs and building inspection fees

Unlike a standard property purchase where surveys are often arranged after an offer is accepted, auction buyers need to carry out any surveys before the auction. This is because you are committing to the purchase on the day, with no opportunity to renegotiate based on survey findings afterwards.

A RICS HomeBuyer Report typically costs between £400 and £1,000 depending on the property and surveyor. A full building survey — the most comprehensive option and the one most commonly recommended for older or unusual properties — can cost between £600 and £1,500.

If the property needs specialist reports — for example, damp, structural movement, drainage, or asbestos surveys — each can add several hundred pounds to your pre-auction costs. These costs are not recoverable if you bid but do not win, or if you decide not to bid after reviewing the results.

Administration fees and additional charges from the auction house

In addition to the buyer’s premium, many auction houses charge separate administration fees. These can include:

- ID verification fees — typically £20 to £50 per buyer, charged to comply with anti-money laundering regulations

- Online bidding fees — some platforms charge an additional fee for remote bidding participation

- Memorandum of sale administration fee — a charge for processing the sale documentation, which can range from £100 to £300

- Buyer registration fees — a minority of auction houses charge a registration fee simply to participate in the auction

These charges are usually set out in the auction house’s terms and conditions document, which is published before the auction. Reading this carefully is just as important as reviewing the legal pack for any specific property.

Special conditions of sale: the hidden property auction fees

One of the most common ways auction buyers find themselves with an unexpectedly high bill is through the Special Conditions of Sale attached to individual lots. These are additional contractual terms that go beyond the standard conditions of sale and are specific to that property.

Special conditions can require the buyer to pay some or all of the following:

- The seller’s legal fees — a common clause that can add £1,000 to £2,500 to the buyer’s total cost

- Searches carried out by the seller’s solicitor — even if you have had your own searches done

- Auction house administration charges on behalf of the seller

- Penalties for late completion, which can be substantial if the buyer misses the 28-day deadline

Because these conditions are buried in the legal pack rather than advertised in the property listing, many buyers do not discover them until after they have won the bid. A thorough pre-auction legal review by an experienced solicitor will identify all of these obligations before you commit. To get an idea of the total legal costs involved, you can use the conveyancing fee calculator to generate an instant estimate for your transaction.

How to budget accurately for buying at property auction

Buying at property auction can be an excellent way to acquire property — but only when you enter the process with a clear understanding of the full cost. Property auction fees extend well beyond the hammer price, and the compressed completion timescales mean there is no room for financial miscalculation once the hammer falls.

Before you bid, add up the following for any property you are seriously considering:

- The hammer price — your maximum bid

- Buyer’s premium — typically 1%–5% plus VAT of the hammer price

- 10% deposit — payable on the day

- Pre-auction legal pack review fee — £150 to £400 plus VAT

- Post-auction conveyancing fees — £800 to £1,800 plus VAT and disbursements

- Stamp duty land tax — calculated on the purchase price using the current SDLT rates

- Land Registry fees — based on the property value

- Survey costs — from £400 to £1,500 depending on the type of survey

- Any seller’s costs or administration charges set out in the Special Conditions of Sale

When these figures are combined, the true cost of buying at property auction is frequently 5% to 10% higher than the hammer price alone. Understanding this in advance — and having all your finances in place before auction day — is the foundation of a successful auction purchase.

Need help understanding property auction fees before you bid?

The real cost of buying at auction can go well beyond the hammer price. From legal fees and

SDLT to buyer’s premiums, reservation fees and special-condition charges, it is important to

understand the full picture before committing to a purchase.

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

Help! the council won’t fix the damp and mould in my council house

-

What is ground rent and should you be concerned?

-

Awaab’s Law Explained: How a tragedy changed the rights of every social housing tenant in the UK