How much deposit do you need to buy a house in the UK?

The deposit to buy a house in the UK is one of the biggest financial decisions you will make. Whether you are a first-time buyer or moving up the property ladder, getting your deposit strategy right can save you thousands of pounds over the life of your mortgage.

This guide explains exactly how much house deposit amount you are likely to need, how deposit size affects your mortgage rate, what options are available to first-time buyers, and the additional costs you must factor in before you exchange contracts.

What is the minimum deposit to buy a house in the UK?

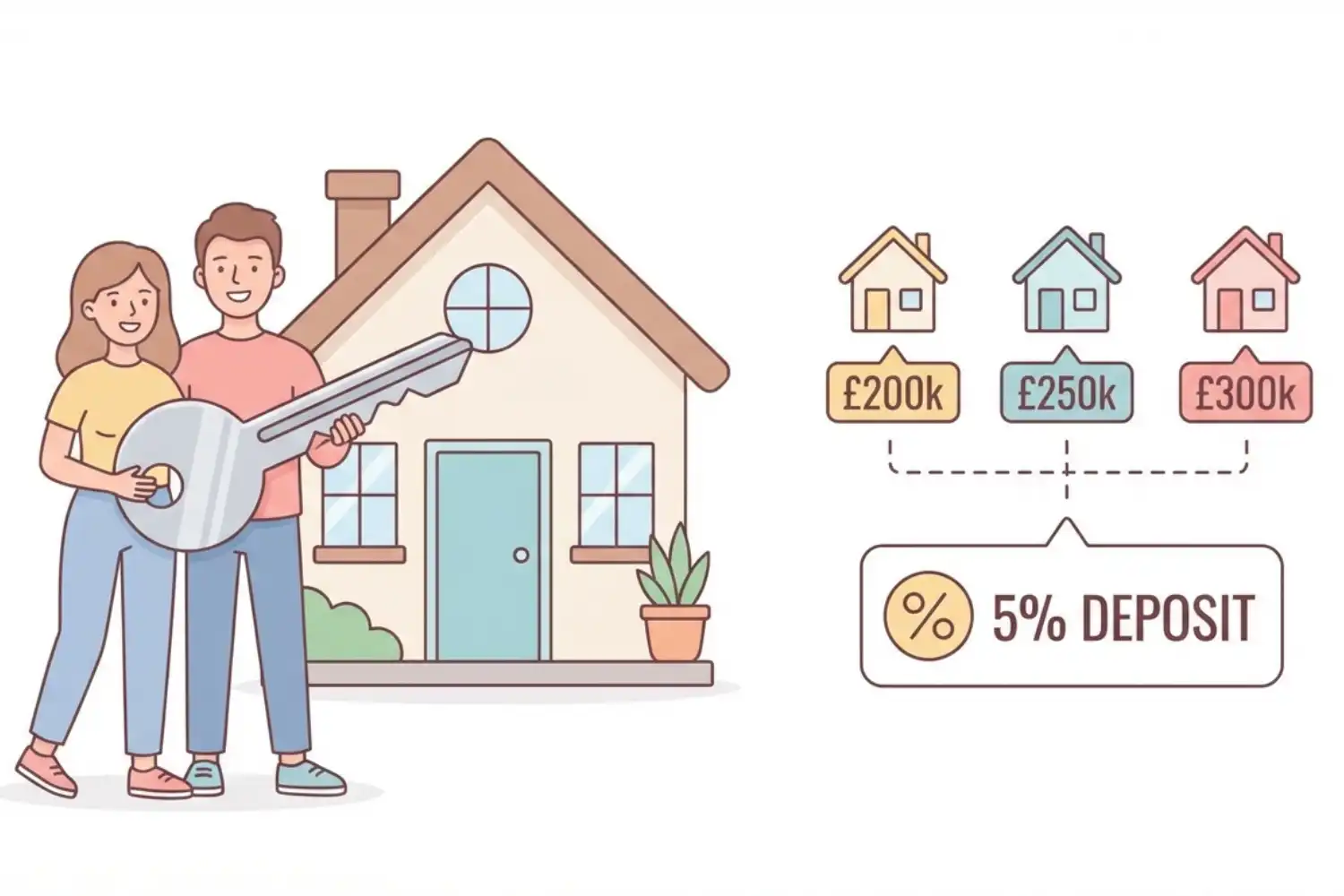

The minimum deposit to buy a house in the UK is typically 5% of the property’s purchase price. This is referred to as a 95% Loan-to-Value (LTV) mortgage — meaning you borrow 95% of the property’s value and contribute the remaining 5% yourself.

To put that in practical terms:

- £200,000 property → 5% deposit = £10,000

- £250,000 property → 5% deposit = £12,500

- £300,000 property → 5% deposit = £15,000

- £400,000 property → 5% deposit = £20,000

While a 5% deposit gets you on the ladder, it is worth understanding that a higher deposit almost always leads to a better mortgage deal. Lenders reward borrowers who contribute more of their own money with lower interest rates, smaller monthly payments and a wider choice of mortgage products.

How does your house deposit amount affect your mortgage rate?

Your deposit size directly determines your Loan-to-Value ratio. The lower your LTV, the lower the risk for the lender — and that reduced risk is usually passed back to you in the form of better interest rates.

Here is how LTV tiers typically affect the mortgage rates available to you:

- 5% deposit (95% LTV): You will face the highest interest rates available. Monthly repayments will be at their largest and you will have a limited choice of lenders.

- 10% deposit (90% LTV): Rates begin to improve. A 10% deposit is a meaningful step up and opens up a noticeably wider range of products.

- 25% deposit (75% LTV): Rates become considerably more competitive. This is often considered the first threshold where meaningful savings start to accumulate.

- 40% deposit (60% LTV): The most favourable rates are typically available at this level. If you can reach 40%, the long-term savings are substantial.

Saving a larger deposit before you buy is often far more financially efficient than getting on the ladder as quickly as possible with the minimum amount. The difference in monthly payments and total interest paid over a 25-year term can easily run to tens of thousands of pounds.

How much is the average first-time buyer deposit in the UK?

The average first-time buyer deposit in the UK has risen significantly in recent years. According to Halifax data, the average first-time buyer deposit was around £61,090 in 2024, representing roughly 20% of the average purchase price.

First-time buyer deposits vary considerably across regions:

- London: average deposit of £124,688

- South East: around £61,744

- South West: around £55,083

- North West: around £39,574

- North East: around £30,678

- Northern Ireland: around £37,898

These figures highlight how regional property prices shape the first-time buyer deposit required. In London and the South East, the gap between income and property prices makes saving a substantial deposit particularly challenging — which is why government schemes and family support have become such an important part of how buyers enter the market.

Unsure if your deposit is enough to buy a property?

Understanding how much deposit you need is only part of the process. Our conveyancing team can help you prepare for the legal stages of buying a home, explain the costs involved, and ensure everything is in place before you exchange contracts.

Ways to boost your deposit to buy a house in the UK

If your current savings do not yet meet the deposit you need, there are several legitimate and widely used options to help you build it faster or stretch what you have.

Lifetime ISA (LISA)

A Lifetime ISA allows you to save up to £4,000 per year towards your first home. The government adds a 25% bonus on top of your contributions — meaning up to £1,000 free each year. To qualify, you must be between 18 and 39 when you open the account, and the property must cost no more than £450,000.

Gifted deposit

A gifted deposit is money given to you by a family member — most commonly a parent — to use as all or part of your deposit to buy a house in the UK. The lender will require written confirmation that the money is a gift and not a loan, usually in the form of a gifted deposit letter. Your solicitor will help ensure the documentation is in order.

Shared ownership

Under shared ownership, you buy a share of a property — typically between 25% and 75% — and pay rent on the remaining share. Crucially, you only need to raise a 5% deposit on the share you are purchasing, not the full property value. This can significantly reduce the deposit required to get onto the ladder.

100% mortgages and guarantor mortgages

It is possible, in limited circumstances, to buy a property without any deposit at all. Some lenders offer 100% mortgages — most notably Skipton Building Society’s Track Record mortgage, designed for renters who have a strong history of paying rent on time. Guarantor mortgages, where a parent or family member uses their savings or property as security, are another route available to some first-time buyers.

Both options carry risk and should be discussed carefully with a qualified mortgage adviser before proceeding.

The exchange deposit: an important distinction when you buy a house in the UK

There is often confusion between the mortgage deposit — the amount your lender requires — and the exchange deposit, which is a separate and equally important figure.

When contracts are exchanged, you are required to pay a deposit to the seller’s solicitor. This is typically 10% of the purchase price, regardless of how large or small your mortgage deposit is.

This creates a practical problem for buyers who are purchasing with a 5% mortgage deposit to buy a house in the UK. If you are only contributing 5% of the property price as your mortgage deposit, you will still need to fund a 10% exchange deposit — which means bridging a 5% gap from somewhere else.

In practice, there are several ways this is handled:

- Using savings to cover the shortfall between your mortgage deposit and the exchange deposit

- Negotiating with the seller (via solicitors) to agree a reduced exchange deposit equal to your actual mortgage deposit

- Using a gifted deposit from family members to top up to the required 10%

This is one of the reasons why working with experienced residential conveyancers matters. The solicitors in our residential conveyancing team routinely guide buyers through the exchange deposit process and help negotiate the most straightforward path to completion.

Deposit requirements for buy-to-let and second homes

The house deposit amount required changes significantly if you are buying a property that is not your primary residence.

- Buy-to-let properties: Most lenders require a minimum 25% deposit for a buy-to-let mortgage, though some may ask for more depending on the rental yield and your financial profile.

- Second homes: If you are purchasing a second residential property, you will generally need at least a 25% deposit.

- New build properties: Lenders often require a larger deposit for new builds — particularly flats. Some lenders require 10–15% even when a 5% product might otherwise be available. Schemes like Deposit Unlock can help bridge this gap for eligible new build purchases.

Extra costs to budget for alongside your deposit

Saving your deposit to buy a house in the UK is a significant achievement — but it is important to remember that the deposit itself is not the only upfront cost you will face. First-time buyers in particular are sometimes caught out by the range of additional expenses that come alongside the purchase.

Key costs to budget for in addition to your deposit include:

- Stamp Duty Land Tax (SDLT): First-time buyers pay no stamp duty on the first £300,000 of a property up to £500,000 in value. Above these thresholds, rates apply. Home movers pay stamp duty at rates starting from £250,001 upwards. Always check current SDLT rates before proceeding, as thresholds can change.

- Solicitor and conveyancing fees: You will need a qualified solicitor to handle the legal side of your purchase. Fees vary depending on the property value, whether it is freehold or leasehold, and the complexity of the transaction.

- Survey costs: A mortgage valuation is not the same as a full structural survey. Depending on the age and condition of the property, a HomeBuyer Report or full Building Survey is strongly advisable and costs extra.

- Mortgage arrangement fees: Some mortgage products carry arrangement or product fees. These can sometimes be added to the mortgage, but doing so increases the total interest you pay.

- Removal costs and initial repairs: Do not forget the practical costs of moving and any immediate work the property needs before it is fully liveable.

What happens to your deposit when you exchange contracts?

Once your house deposit amount is ready and your mortgage has been agreed in principle, the purchase moves towards exchange of contracts. At the point of exchange, your deposit is transferred to the seller’s solicitor by your own conveyancer. The transaction becomes legally binding at this point — if you pull out after exchange, you risk losing your deposit entirely.

This is why the period between receiving your mortgage offer and exchanging contracts is so important. Your solicitor will carry out property searches, review the title, and raise any queries with the seller’s solicitor. Issues identified at this stage can affect the timeline significantly.

Understanding what those searches involve and how long they take is helpful when you are planning timelines. Our article on what searches take the longest when buying a house explains the process clearly so you know what to expect after your offer is accepted.

Tips for saving the deposit to buy a house in the UK more quickly

Building your deposit to buy a house in the UK takes time and discipline, but there are practical ways to accelerate your savings:

- Clear any high-interest debts first — credit cards and personal loans erode your savings capacity every month they remain outstanding

- Open a Lifetime ISA if you are under 40 and have not owned property before — the 25% government bonus is essentially free money towards your first-time buyer deposit

- Set up a dedicated savings account for your deposit and automate monthly transfers so the savings happen before you spend

- Review your regular outgoings — subscriptions, switching energy or insurance providers, and cutting non-essential spending can each add meaningfully to your monthly saving rate

- Consider whether a gifted deposit from family could either accelerate your timeline or help you reach a higher LTV tier with better mortgage rates

If you are further along in your planning and want to understand the purchase process more fully, our guides on spotting issues before you commit are worth reading. We cover what property searches reveal, the signs that can indicate problems with a purchase, and what buyers should be thinking about from the moment their offer is accepted.

For example, our guide on how to spot red flags when buying a house walks through the warning signs that experienced conveyancers look out for — issues that could affect your purchase timeline, your costs, or the value of the property itself.

Ready to take the next step? Talk to a conveyancer

Once your deposit to buy a house in the UK is in place and your mortgage is agreed, the legal process begins. Having a clear, experienced conveyancing team from the start makes a significant difference to how smoothly the transaction progresses.

At Versus Law, our conveyancers are experienced in guiding buyers through every stage of a residential purchase — from the moment an offer is accepted through to the day you receive your keys. If you would like to understand the legal costs involved before you commit, our conveyancing fee calculator provides an immediate, transparent quote with no obligation.

Whether you are a first-time buyer taking your first steps onto the property ladder or an experienced mover working through a more complex chain, our team is ready to help. Get in touch with Versus Law to discuss your purchase and find out how we can support you through the process.

Ready to buy a property in the UK?

Our conveyancing solicitors can guide you through the legal process once your deposit and mortgage are in place. From reviewing contracts to completing searches and managing exchange and completion, we ensure your property purchase progresses smoothly and securely.

-

Why do people avoid leasehold properties?

-

Home insurance – do I need it?

-

Estate agent fees explained: what UK sellers really pay

-

What is joint tenancy vs tenants in common?

-

What are service charges and what do they cover?

-

What happens if a conveyancing search reveals a problem?

-

Can you pull out before exchange of contracts?

-

Property Auction vs Estate Agent: Which Is Really the Better Way to Sell in Manchester?

-

What Fees Do You Pay When Buying at Property Auction? The Full Breakdown

-

Help! the council won’t fix the damp and mould in my council house